LendingTree, a leading online marketplace for financial products, recently highlighted alarming trends in American personal finance through a survey conducted via its subsidiary DepositAccounts. This comprehensive study of 2,000 U.S. consumers reveals deep vulnerabilities in household cash savings, with 37% reporting less than $500 in liquid reserves and 14% having zero savings at all.

What Exactly Is LendingTree and How Does It Operate?

LendingTree is not a direct lender but an innovative online marketplace founded in 1996 by Doug Lebda in Charlotte, North Carolina. After struggling with his own mortgage process, Lebda created a platform where consumers can compare multiple offers from hundreds of lenders side-by-side for products like mortgages, personal loans, auto loans, credit cards, home equity lines, insurance, and deposit accounts. The famous tagline “When banks compete, you win” captures its core mission: empowering shoppers to find better rates and terms without visiting multiple banks.

Through its network of over 300 lenders and 700+ partners, LendingTree has helped 149 million people and facilitated $297 billion in loan funding over 30 years. It also owns DepositAccounts.com, a site focused on high-yield savings, CDs, and banking comparisons — the very platform that published this cash savings study. Users simply answer a few questions, receive personalized offers, and choose the best one, often saving significant money on major financial decisions. The company earns revenue when consumers connect with lenders, but it emphasizes education through expert articles and tools.

Imagine walking into a car dealership where every salesperson competes aggressively for your business — that’s the LendingTree model for loans and banking. One user story shared in financial forums describes a borrower who compared mortgage rates and shaved thousands off closing costs in minutes, turning a stressful process into a smart win.

The Survey Details: A Clear Snapshot of American Cash Savings in 2026

Conducted by QuestionPro for LendingTree/DepositAccounts from February 13-17, 2026, the online survey polled 2,000 Americans aged 18-80 using a representative sample with quality controls. “Cash savings” included checking/savings accounts, money market accounts, CDs, non-retirement brokerage cash, and even cash kept at home.

Key verified facts:

- 37% have less than $500 in cash savings, including the 14% with no savings whatsoever.

- Another 32% have some savings but under $1,000, meaning nearly 7 in 10 Americans lack a meaningful buffer.

- 66% dipped into savings in the past year, often for everyday essentials like food, utilities, or emergencies.

- 29% now have less saved than a year ago (vs. 25% with more), signaling widespread erosion.

- 45% could not cover more than one month of essentials if income stopped; only 21% could last over six months.

- Demographics hit hardest: 32% of those earning under $30,000 have zero savings; 20% of women; 16% of Gen Z.

Matt Schulz, LendingTree’s chief consumer finance analyst, noted: “Stubborn inflation, still-high interest rates, a shaky job market and general economic uncertainty are making things challenging… When prices rise and budgets tighten, something has to give, and often that something might be their savings.”

Skinny Piggy Bank Stock Illustrations – 17 Skinny Piggy Bank Stock Illustrations, Vectors & Clipart – Dreamstime

A skeletal piggy bank symbolizes the fragile state of many American emergency funds, with ribs showing after repeated withdrawals for daily costs (Source: Dreamstime stock illustration).

“Broke” stamped piggy bank — a stark visual of the 14% with zero cash savings facing immediate financial risk (Source: Dreamstime).

What This Cash Savings Crisis Really Means for Everyday Americans

The implications of these cash savings numbers go far beyond statistics — they expose a frayed financial safety net in an era of persistent inflation and economic pressures. With 66% of households tapping reserves just to cover groceries or bills, many live one car repair or medical issue away from debt spirals. Relying on credit cards as a backup (as Schulz warns) becomes dangerous when interest rates remain elevated, turning small setbacks into long-term burdens.

This survey underscores a broader shift: more Americans are seeing savings shrink than grow, despite high-yield options offering better returns than traditional bank accounts. Lower-income groups, women, and younger adults face disproportionate risks, highlighting how cost-of-living increases disproportionately erode cash savings buffers. In a society where unexpected expenses like home repairs or job loss hit frequently, lacking even $500 means heightened stress, delayed goals, and greater reliance on high-cost borrowing.

Yet the data also reveals opportunity. Those building cash savings — even modestly — gain resilience. The 21% who could weather six months demonstrate that deliberate habits create stability.

An older man staring into an empty wallet captures the anxiety many feel when cash savings run dry during uncertain times (Source: Moneytalksnews stock photo).

Woman holding cash with a worried expression — reflecting the emotional toll when low cash savings force tough daily choices (Source: stock image).

Humorous (Yet Telling) Episodes That Highlight the Cash Savings Struggle

Financial vulnerability often breeds relatable, if bittersweet, stories. One viral anecdote involves a millennial who celebrated a small raise by treating friends to dinner — only to realize days later that the “splurge” wiped out their entire emergency fund, leaving them scrambling when their laptop died. “I went from feeling rich to ramen-rich in 48 hours,” they joked online.

Another classic: the Gen Z worker who kept “savings” in a Venmo balance (a habit noted in the survey, popular among younger respondents). When a surprise vet bill hit for their dog, the funds vanished instantly — turning a cute pet photo op into a cautionary tale about treating digital wallets like true cash savings.

Then there’s the Baby Boomer who proudly kept cash “under the mattress” (27% in the survey do something similar), only for inflation to quietly erode its value while high-yield accounts elsewhere grew. These light-hearted stories mask a serious point: without intentional cash savings strategies, life’s curveballs hit harder.

A personal favorite from forums: a couple who used LendingTree to refinance and redirect monthly savings into a high-yield account. Months later, their growing balance funded an impromptu vacation — proof that smart comparison shopping can directly boost cash savings.

Couple reviewing finances on a smartphone — similar to how users compare offers on LendingTree or DepositAccounts to protect and grow cash savings (Source: Bankrate stock photo).

Hands interacting with a mobile banking app — modern tools that help monitor and build cash savings efficiently (Source: Bankrate).

Actionable Insights: Turning Low Cash Savings into Strength

While the survey paints a challenging picture, experts like Schulz offer practical paths forward. Open a high-yield savings account (rates, though lower than peaks, still beat traditional banks). Automate transfers so saving happens without willpower. Revisit your budget to track spending on essentials. Even while paying down debt, maintain some cash savings to avoid new borrowing cycles.

Start small: many who increased monthly contributions did so by under $250. The goal? Build toward 3-6 months of expenses — the classic emergency fund benchmark that only a minority currently meet.

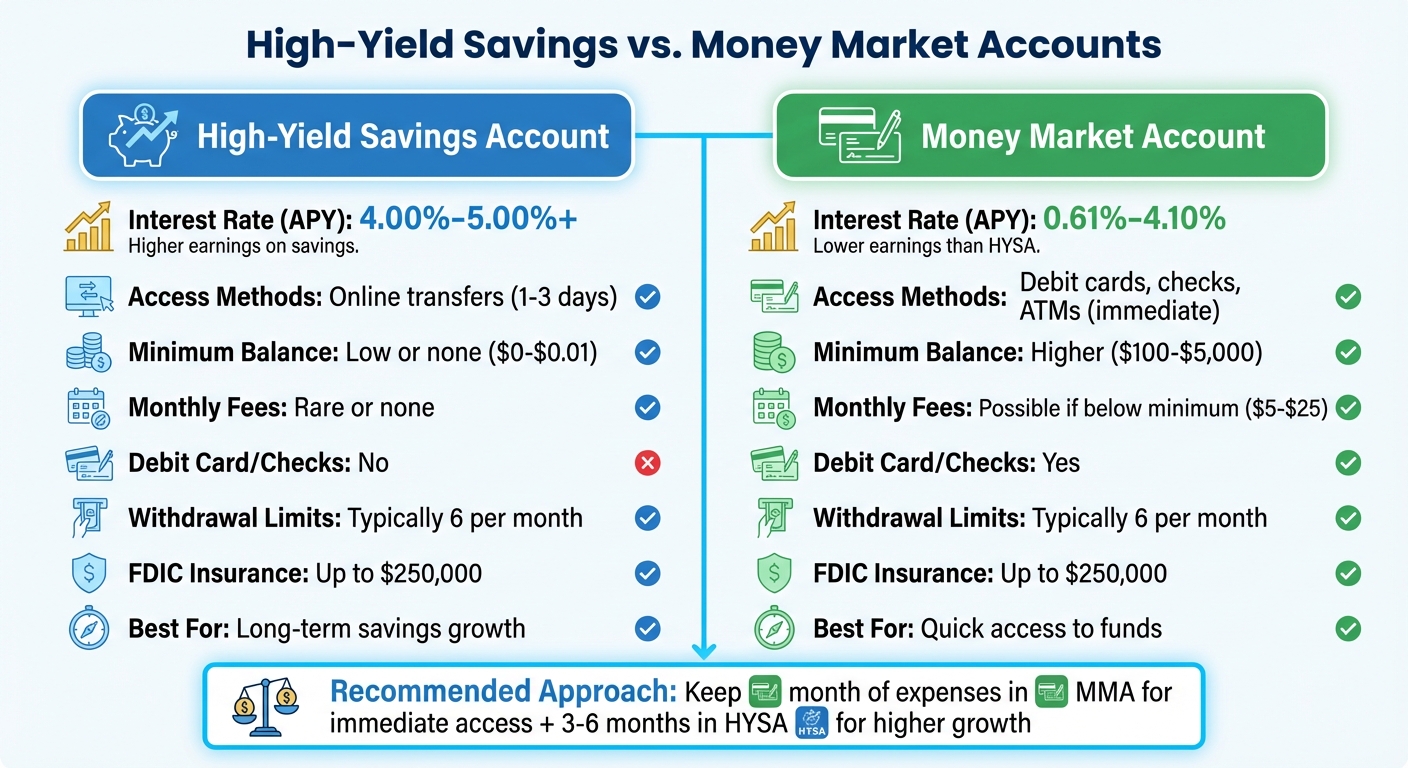

Infographic comparing high-yield savings vs. money market accounts — a useful visual for choosing where to park growing cash savings (Source: Monefy).

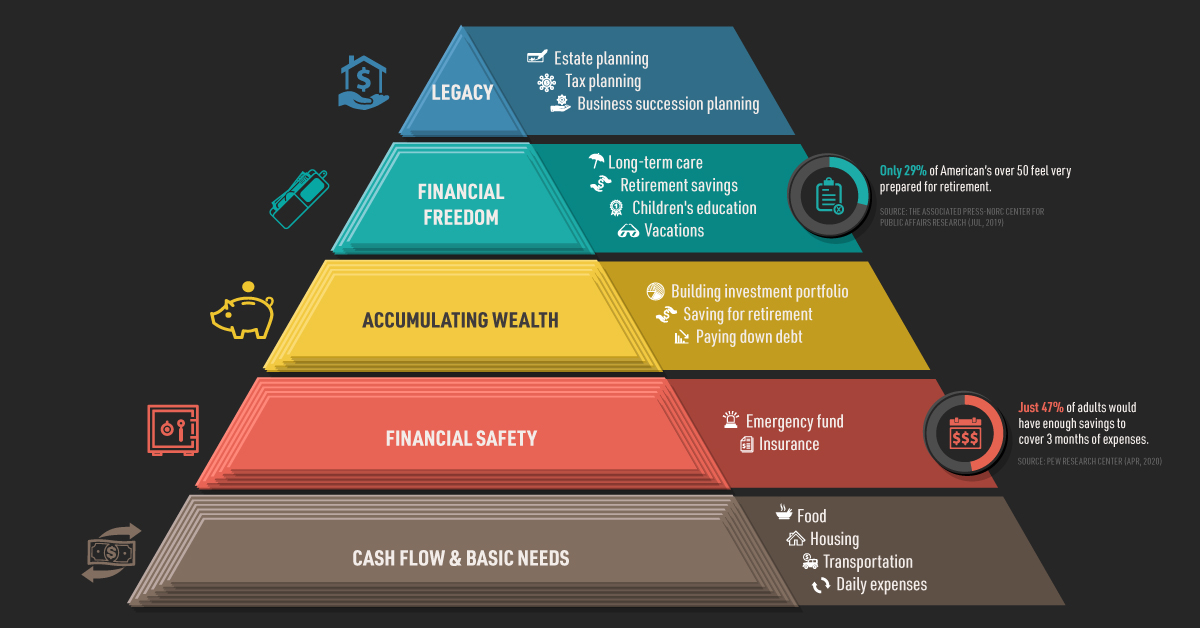

Hierarchy of financial needs pyramid — showing how cash savings forms the base of long-term security (Source: Visual Capitalist adaptation).

Why This Matters Now and How LendingTree Fits In

In 2026, with living costs still pressuring budgets, this LendingTree-backed survey serves as a wake-up call rather than doom-scroll material. It highlights the value of tools like LendingTree and DepositAccounts for comparing not just loans but also better banking options to grow cash savings. By shopping smarter, consumers can free up money that might otherwise vanish.

The survey’s transparent methodology adds credibility — it’s not hype but a clear-eyed look at real household realities.

For the full report, visit the original source: https://www.depositaccounts.com/blog/cash-savings-study.html. Learn more about LendingTree at https://www.lendingtree.com/.

This analysis draws strictly from verified public data and aims to provide balanced, actionable context for personal finance discussions.