In an era when skyrocketing home prices and stubborn mortgage rates have pushed the American Dream further out of reach for millions, Trump’s 50-Year Mortgage Policy has emerged as one of the most talked-about proposals to restore Housing Affordability. Announced in November 2025 and actively evaluated by the Federal Housing Finance Agency (FHFA), this initiative aims to introduce extended-term loans backed by government-sponsored enterprises like Fannie Mae and Freddie Mac. By stretching repayments over half a century, Trump’s 50-Year Mortgage Policy promises dramatically lower monthly payments, potentially unlocking homeownership for first-time buyers and middle-class families squeezed by today’s market realities.

(Image: President Donald Trump addressing housing and economic policies, highlighting his focus on making homeownership more accessible through innovative financing like the proposed 50-Year Mortgage. reuters.com)

This isn’t just another policy tweak—it’s a deliberate evolution of America’s century-long experiment with mortgage finance. Below, we dive deep into the verified history, current landscape, mechanics of a 50-Year Mortgage, the strategic purpose behind Trump’s 50-Year Mortgage Policy, intriguing historical episodes that shaped our system, and forward-looking trends for the real estate market. All facts are drawn from official reports, economic analyses, and government data as of February 2026.

The Evolution of U.S. Real Estate Mortgages: From Balloons to the 30-Year Standard

America’s mortgage system wasn’t always the stable, long-term fixture we know today. Before the 1930s, most home loans were short-term—typically 3 to 5 years—with interest-only payments and a massive “balloon” principal due at the end. Borrowers often refinanced repeatedly, but the Great Depression exposed the fragility of this model. Home prices collapsed, unemployment soared to 25%, and foreclosures skyrocketed, with nearly 10% of mortgaged homes lost between 1931 and 1935.

(Image: Crowds gather during a 1930s farm foreclosure auction amid the Great Depression, illustrating the widespread housing crisis that prompted federal intervention in mortgages. therealnews.com)

Enter the New Deal. In 1933, the Home Owners’ Loan Corporation (HOLC) was created to refinance distressed loans, ultimately aiding nearly one million homeowners and preventing hundreds of thousands of foreclosures. By 1934, the Federal Housing Administration (FHA) began insuring longer-term, fully amortizing loans with down payments as low as 10%. The 30-year fixed-rate mortgage gained traction in 1948 for new construction and expanded in 1954 to existing homes, fueled by postwar VA loans and the need for affordable housing for returning veterans.

A fascinating cultural bridge to this long-term mindset came from an unlikely source: Hollywood icon Charlie Chaplin. During World War I, the U.S. government issued 30-year “Liberty Bonds” to fund the war effort. Chaplin starred in the 1918 propaganda film The Bond and personally promoted bond sales on Wall Street, helping raise nearly $17 billion. This public campaign normalized the idea of committing to financial obligations spanning three decades—planting the seed for the 30-year mortgage that would later define American homeownership.

(Image: Charlie Chaplin promoting Liberty Bonds in 1918, a cultural moment that helped Americans embrace long-term financial commitments leading to today’s mortgage norms. doughboy.org)

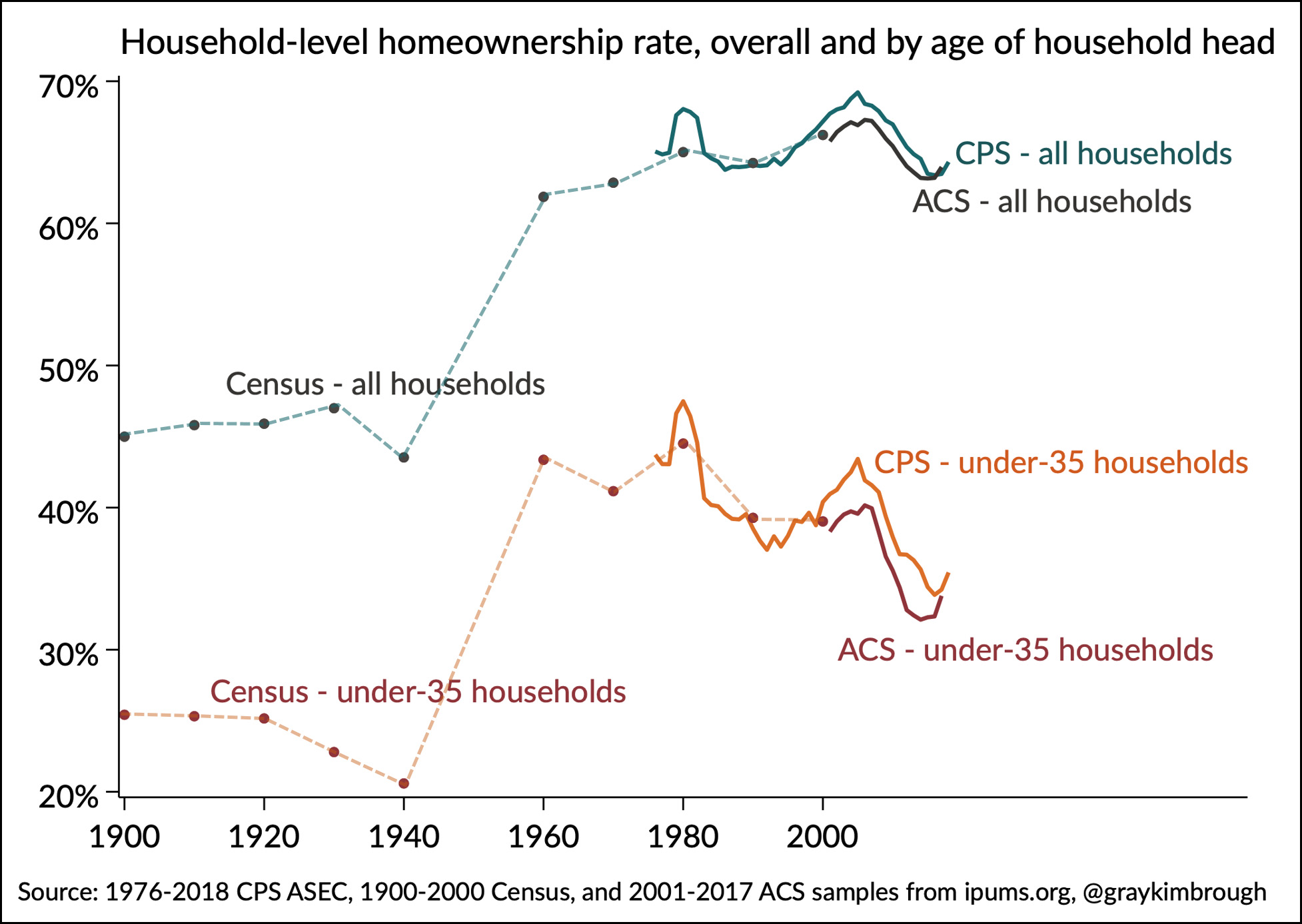

By the 1960s, the 30-year fixed had become the gold standard, backed by Fannie Mae (1938) and Freddie Mac (1970). Homeownership rates surged from 44% in 1940 to 62% by 1960, driven by these innovations. Yet, as recent data shows, the system has struggled with modern affordability pressures.

(Image: Historical chart of U.S. homeownership rates from 1900 to present, showing the dramatic postwar boom enabled by long-term mortgages like the 30-year standard. motherjones.com)

(Image: Classic FHA promotional poster from the New Deal era, emphasizing how small down payments could turn rent into homeownership—a message echoed in today’s discussions of extended mortgage terms. unvarnishedhistory.org)

Today’s Mortgage Landscape in 2026: Options and Realities

As of February 2026, the dominant choices remain the 15-year and 30-year fixed-rate mortgages, with the latter averaging around 6.01% nationally (per Freddie Mac’s Primary Mortgage Market Survey). Adjustable-rate mortgages (ARMs) offer initial lower rates but carry reset risks. True 40-year or longer terms have been rare and mostly available through non-qualified or portfolio loans, not widely backed by government entities—until the recent push under Trump’s 50-Year Mortgage Policy.

Current 30-year rates have improved from 2025 peaks thanks to Federal Reserve easing and the administration’s $200 billion mortgage-backed securities (MBS) purchase directive, but median home prices hover near $397,000, keeping monthly payments burdensome for many.

Breaking Down the 50-Year Mortgage: Pros, Cons, and Cold Calculations

A 50-Year Mortgage would amortize the loan principal and interest over 600 months instead of 360. Using a median home price example of $415,200 (with 20% down and ~6.3% rate), a traditional 30-year payment (principal + interest) sits around $2,056 monthly. Extending to 50 years drops it to approximately $1,823—a savings of roughly $233 per month, according to analyses from Rate.com and ConsumerAffairs.

Pros of the 50-Year Mortgage:

- Sharply lower monthly obligations, improving qualification and cash flow for young buyers or those in high-cost areas.

- Greater purchasing power, allowing families to afford slightly larger or better-located homes.

- Enhanced Housing Affordability in the short term, aligning directly with the goals of Trump’s 50-Year Mortgage Policy.

(Image: Comparative chart illustrating how monthly payments vary across 15-, 30-, and 50-year mortgage terms at different interest rates, underscoring the affordability edge of longer terms. reddit.com)

Cons of the 50-Year Mortgage (verified across UBS, Forbes, and Better.com analyses):

- Dramatically higher lifetime interest—often 2x or more. On the example loan, total interest could exceed $800,000 versus ~$450,000 on a 30-year.

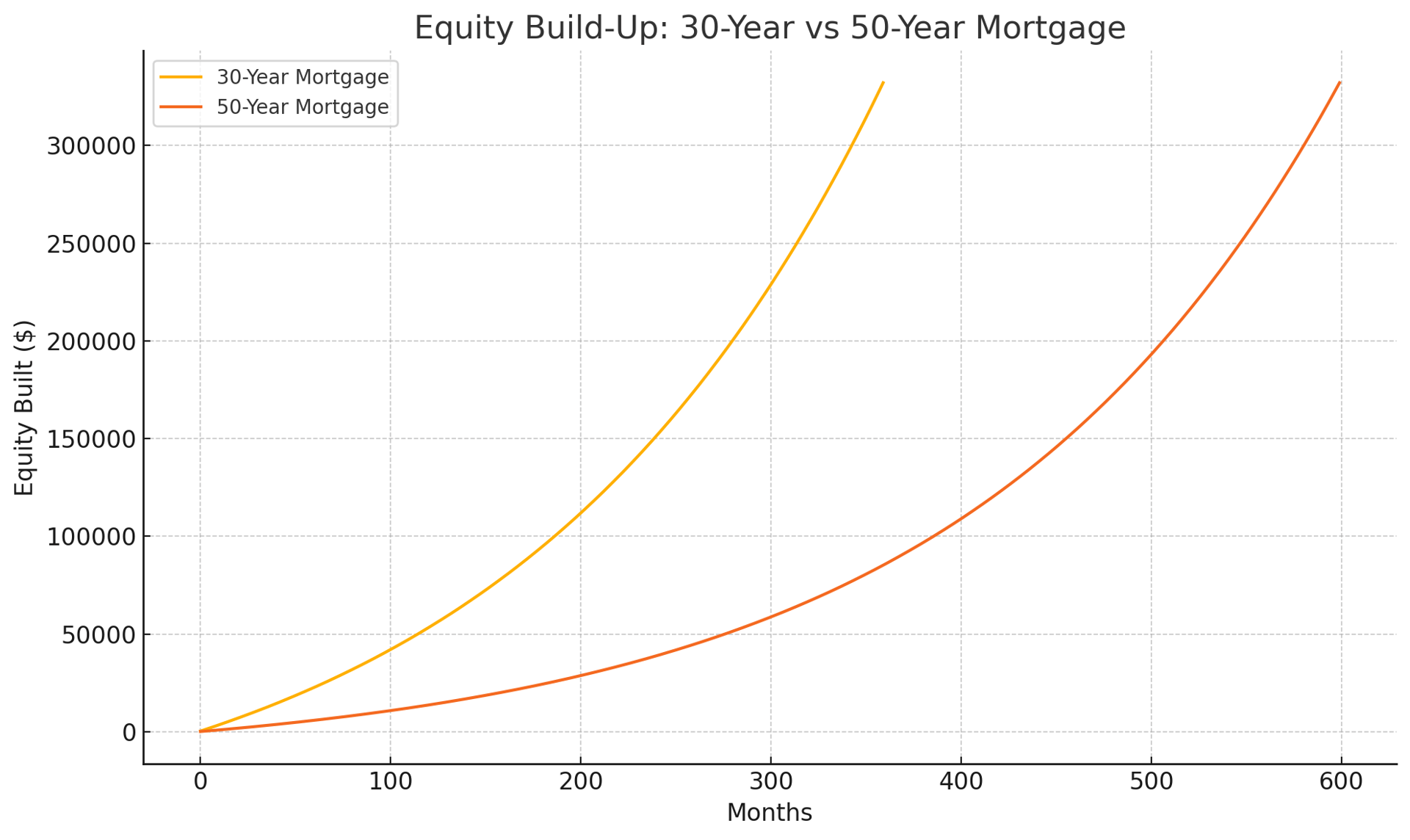

- Slower equity buildup: After 10 years, only ~4% of principal paid off (vs. 16% on 30-year); after 20 years, just 11% (vs. 46%).

- Debt extending deep into retirement years for many borrowers.

- Potentially higher interest rates for the extended risk (0.25–0.75% premium estimated).

(Image: Equity buildup comparison chart between 30-year and 50-year mortgages, clearly showing the significantly slower wealth accumulation with extended terms. ccg-chicago.com)

Critics, including some conservative voices, argue the modest monthly relief doesn’t justify the long-term cost, yet proponents of Trump’s 50-Year Mortgage Policy see it as a pragmatic tool when paired with other measures.

The Strategic Purpose of Trump’s 50-Year Mortgage Policy

Trump’s 50-Year Mortgage Policy isn’t isolated—it’s part of a comprehensive affordability agenda launched in late 2025. FHFA Director Bill Pulte called it a “complete game changer” for lowering barriers. The core purpose: combat post-pandemic price surges (homes up ~75% in a decade) and elevated rates that pushed first-time buyer age to 40. By directing Fannie and Freddie to support these loans, the administration aims to reduce monthly burdens without inflating prices further.

Complementary actions include the January 2026 executive order restricting large institutional investors from snapping up single-family homes and the $200 billion MBS purchase to ease rates. The overarching goal of Trump’s 50-Year Mortgage Policy is clear: expand the ownership society, prioritize families over Wall Street, and restore the middle-class pathway to wealth through home equity.

(Image: President Trump speaking at the World Economic Forum in Davos 2026, outlining broader housing and economic initiatives tied to mortgage innovation. businessinsider.com)

Captivating Episodes That Shaped Mortgage History

Beyond dry facts lie colorful stories. During the Depression, “penny auctions” saw neighbors bid pennies on foreclosed farms to return them to owners—acts of community defiance against banks. The HOLC not only saved homes but inadvertently introduced redlining practices that echo in today’s equity debates. Post-WWII, VA loans with zero-down options fueled suburban sprawl and the baby boom. And who knew a silent-film star’s bond-selling antics helped pave the way for the very 30-year model now being challenged by Trump’s 50-Year Mortgage Policy?

These episodes remind us that mortgage innovation has always been born from crisis and creativity—mirroring the bold thinking behind today’s extended-term proposals.

Future Real Estate Market Trends Under This Policy Horizon

Looking ahead to 2026–2027, forecasts from Fannie Mae, NAR, and Morgan Stanley paint a cautiously optimistic picture. Mortgage rates are projected to stabilize in the mid-5.75% to 6.3% range, with 30-year averages possibly dipping below 6% mid-year. Home prices may rise modestly (~2%), while sales volume could jump 14% as inventory slowly improves.

If fully implemented, Trump’s 50-Year Mortgage Policy could further enhance Housing Affordability for entry-level buyers, potentially accelerating transaction volume in affordable segments. However, experts caution that without supply-side reforms (zoning, construction incentives), the policy risks inflating demand without addressing root shortages. Overall market trajectory: steadier affordability, gradual equity gains for new owners, and a shift toward more inclusive ownership—provided borrowers weigh the long-term math carefully.

(Image: Classic “For Sale” sign in front of a welcoming suburban home, symbolizing the enduring appeal of homeownership that policies like Trump’s 50-Year Mortgage aim to preserve and expand. strategictitle.com)

(Image: Professional real estate “For Sale” sign highlighting modern marketing in today’s competitive housing market. theclose.com)

Final Reflections on a Transformative Proposal

Trump’s 50-Year Mortgage Policy represents a creative, if controversial, response to entrenched Housing Affordability challenges. By building on a century of mortgage evolution—from Depression-era rescues to postwar booms—it seeks to adapt the system for 21st-century realities. While the 50-Year Mortgage offers immediate breathing room, its success will hinge on responsible implementation, borrower education, and complementary supply increases.

Whether this becomes the next chapter in America’s homeownership story remains to be seen, but the conversation it has sparked is already reshaping expectations.